Inflation Expectations and Their Impact on Equities and Bonds

The inflation story of 2026 is not over. Treasury yields are surging, the Fed is on pause, and a new Fed Chair inherits one of the more complicated price environments in recent memory. Here is what investors need to understand right now.

The Inflation Conversation Isn't Over

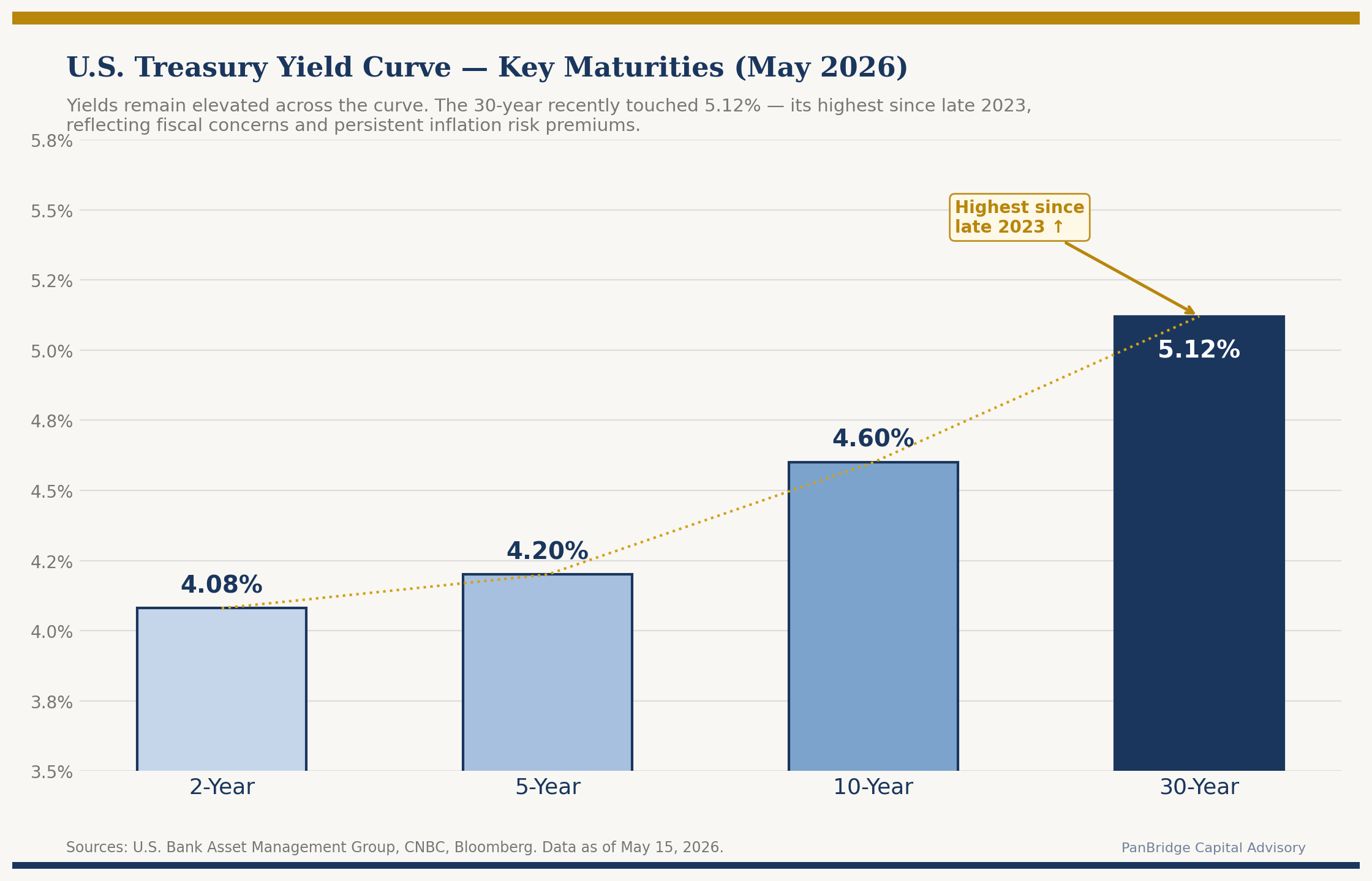

If you assumed inflation was yesterday's problem, the bond market has a different opinion. On May 15, 2026, Treasury yields spiked sharply — the 10-year note surged nearly 14 basis points to 4.595%, and the 30-year bond climbed to 5.121%, its highest level since May 2025. The trigger? A week of messy inflation data and the arrival of new Federal Reserve Chair Kevin Warsh, who now inherits one of the more complicated inflation environments in recent memory.

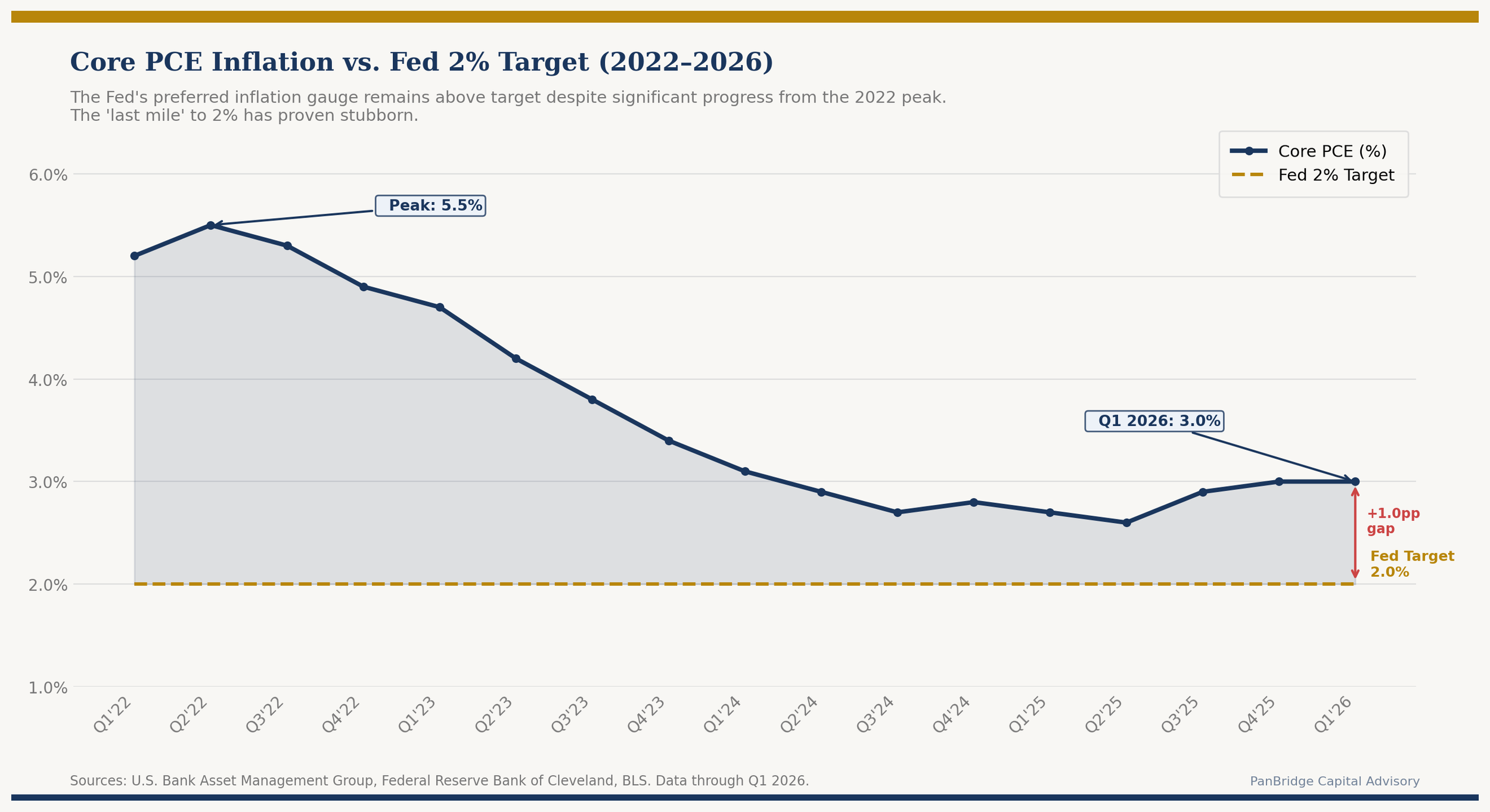

The March Consumer Price Index (CPI) came in at 3.3% year-over-year, with core CPI (excluding food and energy) at 2.6% — still meaningfully above the Fed's 2% target. Core PCE, the Fed's preferred inflation gauge, has eased from a peak above 5.5% in 2022 but remains elevated at approximately 3.0% as of early 2026.

This matters — not just as a headline, but as a direct force shaping how equities are valued and how bonds behave. Understanding the relationship between inflation expectations and asset prices is one of the most important things an investor can internalize right now.

Why Inflation Expectations Matter More Than Inflation Itself

Here is a nuance that many investors miss: markets do not just react to current inflation — they react to where they think inflation is going.

“Markets don’t react to where inflation is. They react to where inflation is going. That distinction is everything for how you position a portfolio.”

When investors expect inflation to remain elevated or reaccelerate, several things happen simultaneously: bond yields rise as investors demand higher compensation for eroding purchasing power; bond prices fall since yield and price move inversely; equity valuations compress — particularly for growth stocks whose future earnings are discounted at a higher rate; and the cost of capital increases for businesses, pressuring profit margins.

Conversely, when inflation expectations fall, the opposite dynamic plays out — yields soften, bonds appreciate, and growth equities tend to rally as discount rates decline. The Federal Reserve's dual mandate — price stability and full employment — means every inflation print carries enormous weight for financial markets.

The Fed's Difficult Position

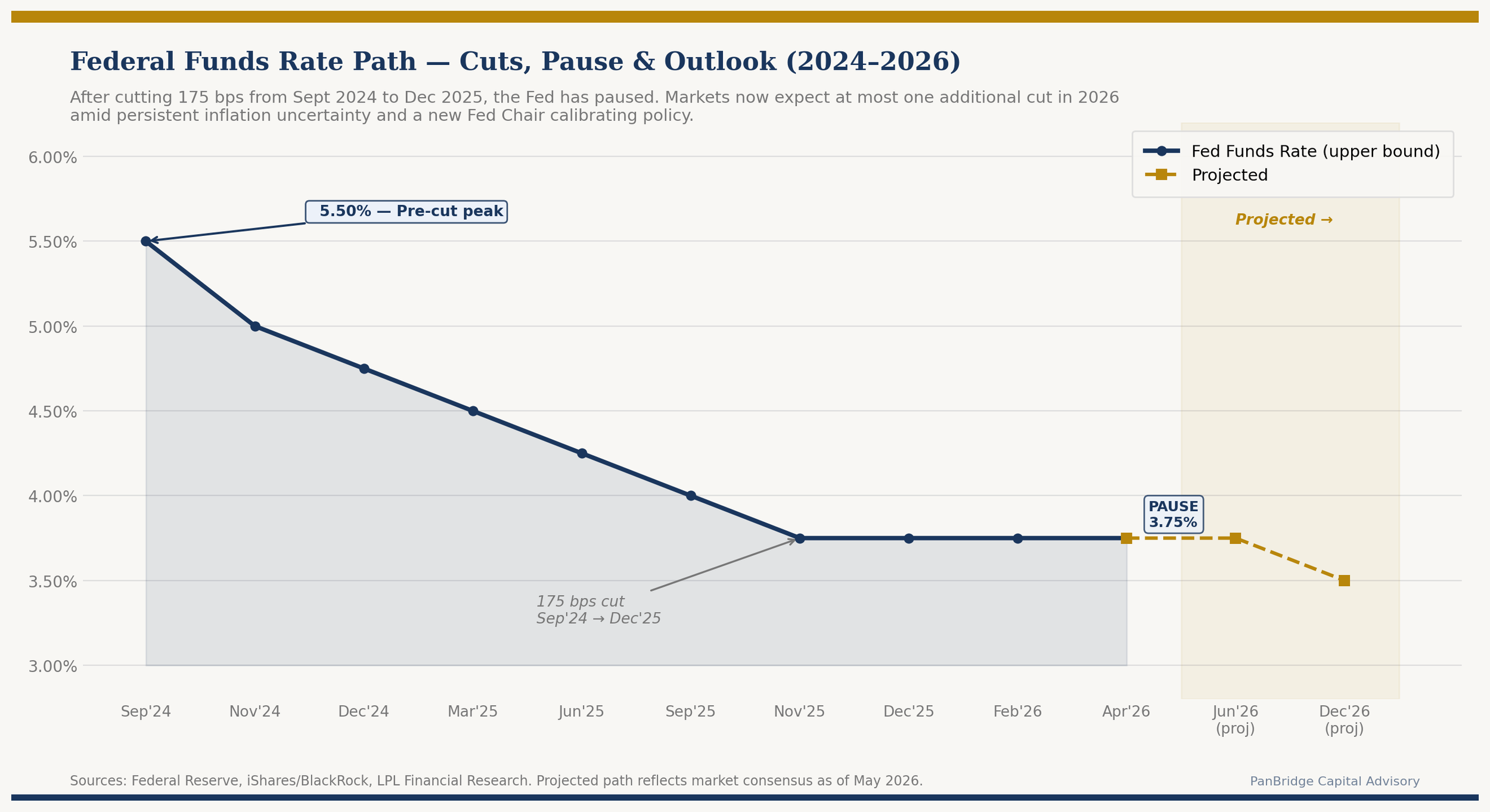

The Federal Reserve cut interest rates by a cumulative 175 basis points between September 2024 and the end of 2025, bringing the federal funds target range to 3.50%–3.75%. Since then, it has paused — holding rates steady at its first three 2026 meetings.

Three reasons for the pause

Inflation above target. Core PCE and CPI are both running above 2%, and geopolitical uncertainty — particularly the Iran conflict and its effect on oil prices — has made the path to 2% less predictable. The March CPI came in at 3.3% year-over-year, with shelter costs still running at 3.0%.

Fed leadership transition. Jerome Powell's term expired in May 2026. New Fed Chair Kevin Warsh now leads the FOMC at a particularly sensitive moment. Markets are still calibrating his policy stance, which adds uncertainty to rate expectations.

Fiscal backdrop. The "One Big Beautiful Bill Act" extends current tax rates and adds new tax cuts while only modestly trimming spending — with the Congressional Budget Office estimating a potential $3.4 trillion increase in federal debt by 2034. Higher deficits mean more Treasury issuance, which puts upward pressure on long-term yields independent of Fed policy.

Impact on Bonds

The bond market is arguably the most direct transmission mechanism for inflation expectations. Here is how different parts of the curve are behaving right now.

Short-term bonds (0–2 years) are most sensitive to Fed policy. With the fed funds rate at 3.50%–3.75%, the 2-year Treasury recently stood near 4.08% — attractive by recent historical standards.

Intermediate bonds (3–7 years) represent the "belly of the curve" — highlighted by several strategists as offering a reasonable yield pickup with manageable duration risk in the current environment.

Long-term bonds (10–30 years) are more sensitive to long-run inflation expectations and fiscal concerns. The 10-year has been in a 3.75%–4.60% range, with the most recent read at 4.595%. The 30-year recently touched 5.121% — territory not seen since late 2023.

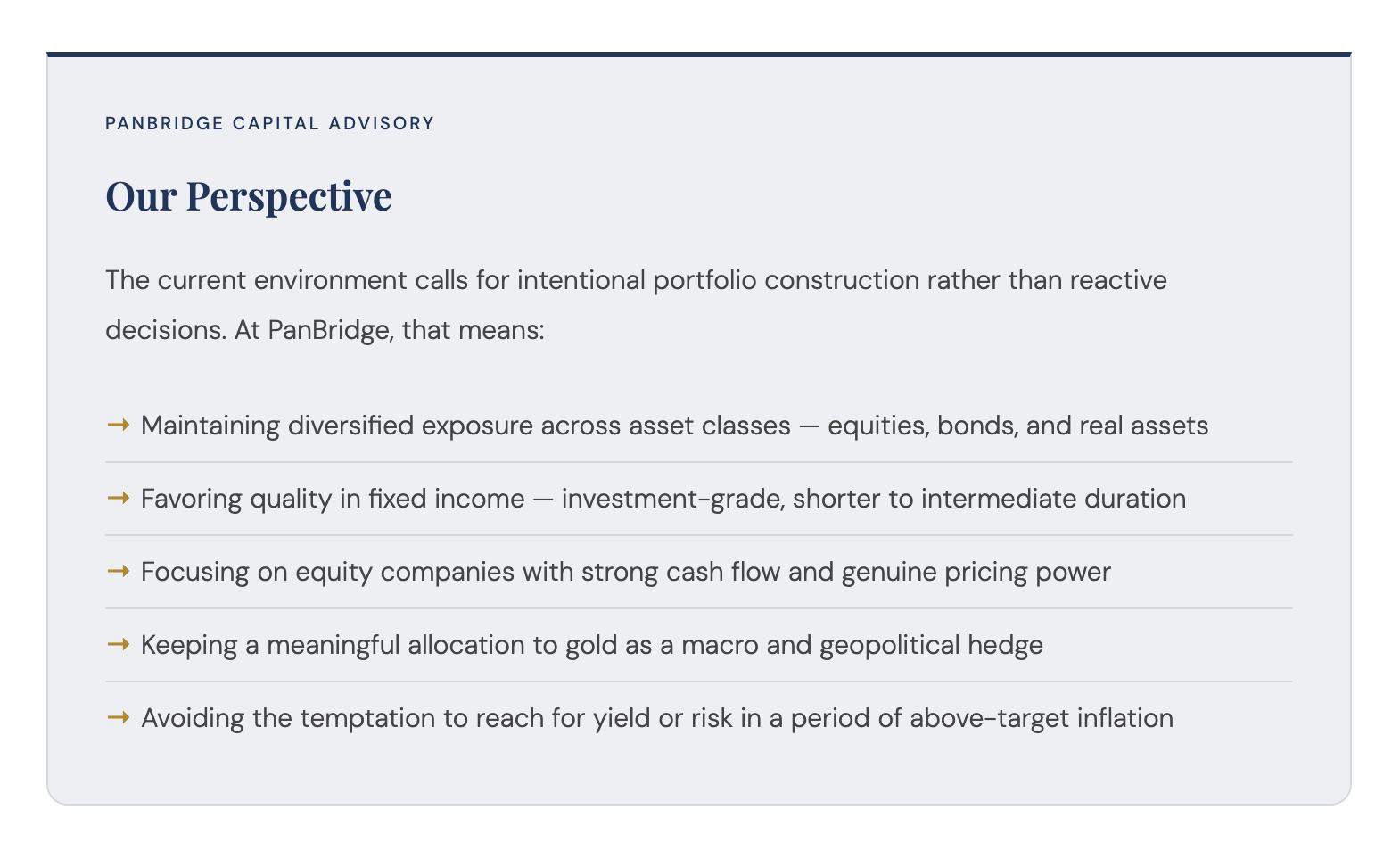

Total returns in 2026 are expected to be income-driven, not price-appreciation driven. Bond laddering — spreading maturities across the curve — is a prudent approach for managing interest rate risk in this environment.

Impact on Equities

The S&P 500 reached a new all-time high of 7,209 as of April 30, 2026 — a signal that corporate fundamentals remain broadly supportive. Yet the relationship between inflation, rates, and equity prices deserves careful attention.

Growth stocks — technology, AI, high-multiple companies — are the most rate-sensitive area of the equity market. When discount rates rise due to inflation expectations, the present value of future earnings declines, compressing valuations. Sector leadership has broadened in 2026 as investors recalibrate, with energy, utilities, industrials, and healthcare gaining ground alongside technology.

Value and dividend stocks tend to be more resilient in inflationary environments. Companies with strong current cash flows, pricing power, and dividend growth offer a degree of inflation protection that high-multiple growth stocks cannot.

Energy stocks deserve particular mention. Given that elevated oil prices are a contributing factor to current inflation uncertainty, energy companies with direct commodity exposure may serve as an inflation hedge within an equity portfolio.

“Despite higher interest rates, solid corporate earnings growth continues to support equity prices — but the path from here is likely to be choppier than the last two years.”

The Gold Factor

No inflation discussion is complete without mentioning gold. As a non-yielding asset, gold tends to perform well when real interest rates (nominal rates minus inflation) are low or negative, and when currency and fiscal concerns are elevated.

With U.S. fiscal deficits widening, inflation remaining above target, and geopolitical uncertainty intensifying, gold remains a relevant component of a well-diversified portfolio — particularly as a hedge against monetary policy uncertainty and structural fiscal pressures. This aligns with a macro-aware investment thesis that recognizes the long-term implications of elevated global debt levels.

The inflation story of 2026 is not a repeat of 2022's shock — but it is also not over. Investors who stay disciplined, diversified, and informed will be best positioned to navigate what remains an uncertain path to price stability.

Educational content only. Not investment advice. Past performance does not guarantee future results. Consult a qualified financial professional for guidance tailored to your specific situation and objectives.

Sources: U.S. Bank Asset Management Group, iShares/BlackRock, LPL Financial Research, RBC Wealth Management, Federal Reserve Bank of Cleveland, CNBC, Vanguard Economic and Market Outlook 2026. Data as of May 2026.